How Immigrants Can Build Credit in the U.S. Fast

Moving to a new country brings big changes. For immigrants settling in the United States, one of the most misunderstood financial challenges is the U.S. credit system. Unlike in many countries, your prior financial history usually doesn’t carry over here. This leaves millions of newcomers with no U.S. credit history—a status known as being “credit invisible.”

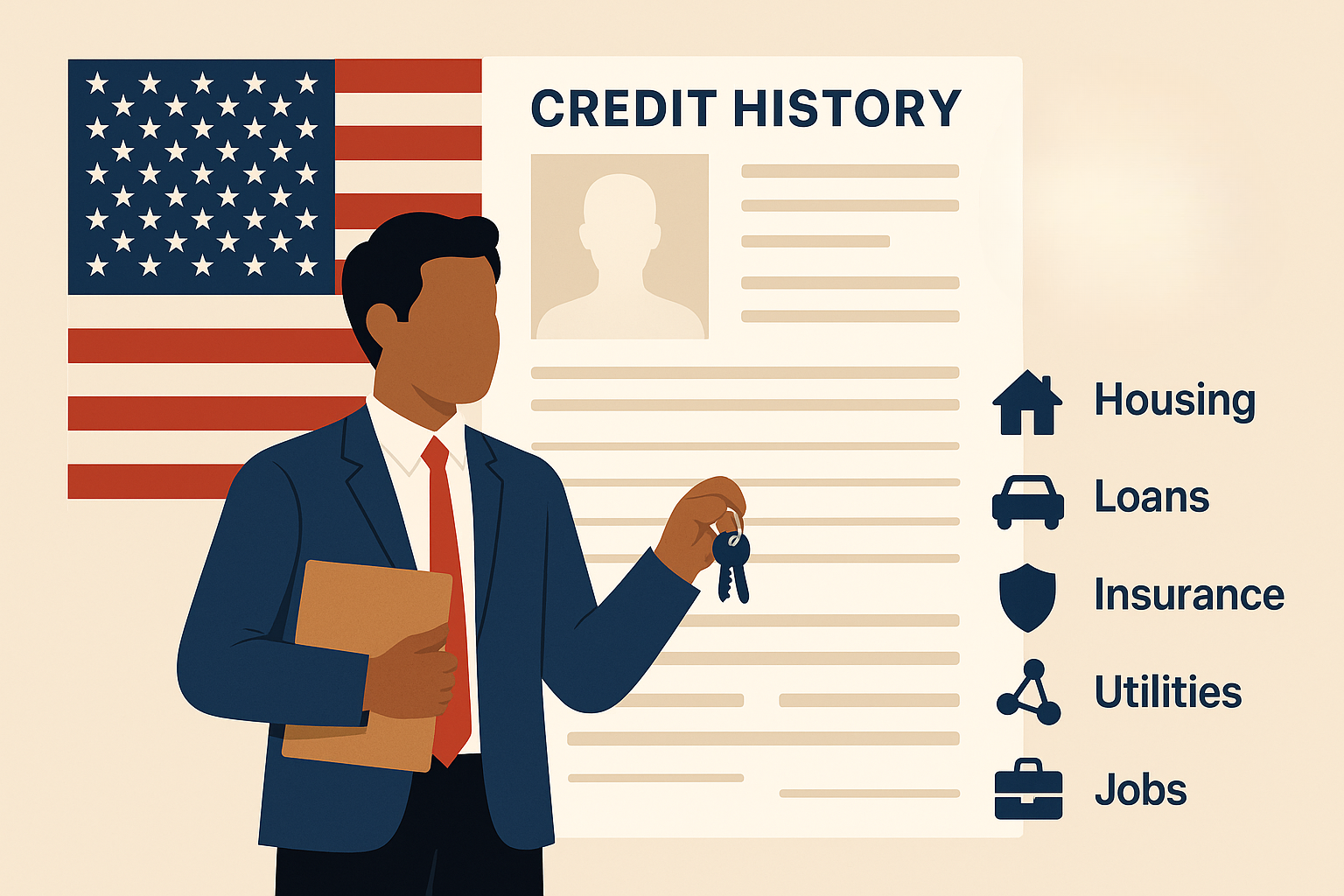

That invisibility can block access to housing, jobs, insurance, loans, and even basic services. But here’s the good news: with a plan, immigrants can build strong personal and business credit in the U.S.—sometimes faster than expected.

Why credit matters more than you think

Credit in the U.S. goes beyond borrowing money. It’s a scorecard that influences your financial life in ways that might surprise you.

- Renting an apartment? Landlords often reject applicants with no credit or demand steep security deposits.

- Buying a car? Lenders charge higher interest rates—or deny financing—without credit history.

- Getting insurance? Companies use credit-based scores to set rates, and no credit usually means higher premiums.

- Setting up utilities? You may have to pay large deposits for internet, electricity, or mobile service.

- Applying for jobs? Some employers check credit reports during the hiring process.

Even simple tasks like signing up for a phone plan can become expensive hurdles.

Understanding the credit timeline

So how long does it take to build credit in the U.S.? It depends on the steps you take, but here’s a general idea:

- First score appears: If you open an account that reports to the credit bureaus, your score could show up in 1–6 months.

- Good score (700+): With consistent, responsible behavior, many immigrants reach a good score within 12–18 months.

- Strong profile: Building a solid history that supports large loans or business financing often takes 2 years or more.

First steps: building personal credit

1. Get your U.S. identification in order

Before anything else, you’ll need either a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). These allow banks and credit bureaus to track your financial activity.

2. Open a U.S. bank account

Even if it doesn’t build credit directly, having a checking and savings account signals that you're active in the financial system. Credit unions and community banks often welcome immigrants with limited documentation.

3. Apply for a secured credit card

This is one of the most popular ways to start building credit. You place a refundable deposit—say $300—and that becomes your credit limit. Use it for small purchases and pay off the full balance every month.

4. Become an authorized user

If a trusted family member or friend adds you to their existing credit card, their payment history could help boost your own credit score. Just make sure they pay on time—otherwise, it could backfire.

5. Try a credit-builder loan

Credit-builder loans are small, safe ways to build credit. You borrow a small amount—like $500—but the bank holds onto it while you make monthly payments. When you’re done, you get the money, and the on-time payments show up on your credit report.

Look into local credit unions or financial institutions.

6. Report Your rent and utilities

Some services let you add rent, phone, or utility payments to your credit report. Since these bills are already part of your life, getting credit for paying them on time can speed up your progress.

Starting a business? You’ll want business credit too

If you’re an immigrant entrepreneur, it’s critical to build business credit that’s separate from your personal finances. This can protect your assets, improve your access to capital, and make your business more attractive to partners.

Here’s how business credit is different:

- Tied to your EIN, not your SSN

- Tracked by business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business

- Publicly viewable, unlike personal credit

Six steps to building business credit

1. Create a legal business entity

Set up your business as an LLC, corporation, or other official structure. Sole proprietorships don’t offer credit separation.

2. Get an EIN (employer identification number)

Apply for one free through the IRS. It acts like a Social Security Number for your business.

3. Open a business bank account

Use your business name and EIN. Avoid using personal accounts for business expenses. This separation is key to building credibility and protecting yourself legally.

4. Set Up Business contact info

Have a dedicated business phone number, email address, and website. Use a real physical address if possible—not just a P.O. box.

5. Start with vendor credit

Open accounts with suppliers or vendors that allow “Net-30” terms (pay within 30 days). Make payments on time and request they report your history to credit bureaus.

6. Apply for a business credit card

Some business cards, like those from Chase or American Express, report to business credit agencies. Use them responsibly—just like personal cards—and never max them out.

A modern option: ramp card for immigrant entrepreneurs

For immigrants launching businesses, one of the biggest challenges is accessing corporate credit without a long personal credit history. Ramp offers a new solution.

Why ramp stands out:

- No personal credit check: Approval is based on your business’s financials, not your personal credit.

- EIN-only application: Great for immigrants with ITINs or no SSN.

- High credit limits: Based on business cash flow and reserves.

- No annual fees or interest: It's a charge card, not a revolving credit card.

- Instant virtual cards: Issue cards with spending limits for employees.

- Built-in expense tracking: Integrates with QuickBooks, Xero, and other platforms.

Businesses usually need to show $25,000–$100,000+ in cash reserves or consistent revenue to qualify. If you meet those standards, Ramp could provide the credit flexibility to grow without putting your personal finances at risk.

Smart timeline for new arrivals

Here’s a month-by-month plan to keep you on track:

First 3 Months

- Apply for SSN or ITIN

- Open personal and (if needed) business bank accounts

- Set up your business structure and EIN

Months 3–6

- Get a secured credit card or become an authorized user

- Apply for Ramp (if eligible) or start building vendor relationships

- Set up utility and rent reporting tools

Months 6–12

- Your first credit score may appear

- Add a credit-builder loan or another secured card

- Pay everything on time—no exceptions

Months 12–24

- Your score should improve into the 700+ range

- Graduate to unsecured cards and better business financing

- Continue building a strong credit mix and long history

The cost of doing nothing

Staying credit-invisible isn’t just inconvenient. It’s expensive.

- Higher deposits: You could pay $1,000+ more upfront for housing and services

- Worse insurance rates: Paying $500 more annually isn’t uncommon

- More expensive loans: A higher interest rate on a car loan could cost you thousands

- Fewer options: No access to reward cards, fraud protection, or emergency credit

Every month you delay building credit, you’re missing opportunities to save money and build a stable life.

Credit is a barrier. Here’s how we help

We just covered how building credit in the U.S. can feel like a maze for newcomers. It slows down everything—access to housing, financial tools, and business growth. That’s exactly why we support our clients through each financial step with clear, guided solutions.

Here’s how we help:

- Business bank account setup: Whether you're going with a virtual provider or a traditional bank, we prepare the documents, guide you through the application, and remain involved until your account is open and ready to use.

- Fund transfers without the headaches: International transfers can eat up time and money. We point you to trusted platforms that offer lower fees, better exchange rates, and faster delivery—so more of your capital goes where it should.

- Corporate credit access from day one: Once your business account is active, we help you apply for a corporate credit card that doesn’t rely on your personal credit. This lets you start building a business credit profile while managing expenses with confidence.

Our team has helped thousands of entrepreneurs and immigrants move to the U.S. quickly, correctly, and with clarity. If you’re looking to do the same, complete our eligibility form and let us make it happen.

Final thoughts

For immigrants, building credit might seem like climbing a mountain—but it’s a climb you can complete faster than you think. It starts with small, consistent steps: secure a credit product, pay on time, watch your balances, and make smart decisions.

If you’re starting a business, the stakes are even higher—but tools like Ramp are changing the game, making credit more accessible and flexible.

With focus and the right tools, you’ll go from invisible to financially empowered—and open the doors you came to the U.S. to unlock.

Discover if you qualify to invest in a thriving U.S. franchise and secure your E-2 visa.

Check your eligibility

More Insights You Might Like

Explore related articles packed with expert advice, real stories, and practical tips to support your U.S. visa and relocation journey.